With 40 licensed holders, Singapore continues to be a key financial center supporting the crypto industry’s growth. The Monetary Authority of Singapore (MAS) has established guidelines to ensure a safe and conducive environment for this sector, including regulations for stablecoins. This supportive regulatory framework has positioned Singapore as a leading hub for crypto startups and innovation. In 2025, to support businesses in Singapore, there are significant tax rebate and cash grants given.

What are the tax incentives provided by the government this year for Web3 Businesses and Individuals?

Budget 2025 – Impact on Web3 Businesses

- To help companies manage rising costs, a CIT Rebate of 50% of tax payable will be granted for YA 2025. The maximum total benefits of CIT Rebate and CIT Rebate Cash Grant that a company may receive is $40,000.

- Extend the Enhanced Cap for the Market Readiness Assistance Grant of $100,000 per new market to help companies to expand into new markets overseas by defraying the costs of overseas market promotion, business development, and market set-up.

- The scope of the EFS – Mergers and Acquisitions Loan will be enhanced beyond equity acquisitions to support targeted asset acquisitions

Budget 2025 – Impact on Web3 Individuals

- In view of cost-of-living concerns, a PIT Rebate of 60% of tax payable will be granted to all tax resident individuals for Year of Assessment (YA) 2025. The rebate will be capped at $200 per taxpayer.

What are the crypto tax rates in Singapore?

Web3 Individuals

Income tax rates depend on an individual’s tax residency status. You will be treated as a tax resident for a particular YA if you are a:

- Singapore Citizen or Singapore Permanent Resident who resides in Singapore except for temporary absences; or

- Foreigner who has stayed/worked in Singapore:

a. For at least 183 days in the previous calendar year; or

b. Continuously for 3 consecutive years, even if the period of stay in Singapore may be less than 183 days in the first year and/or third year; or

- Foreigner who has worked in Singapore for a continuous period straddling 2 calendar years and the total period of stay is at least 183 days*. This applies to employees who entered Singapore but excludes directors of a company, public entertainers, or professionals.

If you do not meet the conditions stated above, you will be treated as a non-resident of Singapore for tax purposes.

Web3 Businesses

Your company is taxed at a flat rate of 17% of its chargeable income. This applies to both local and foreign companies. Foreign income refers to income derived from outside Singapore. Generally, such income is taxable in Singapore when remitted to and received in Singapore. Where the foreign income arises from a trade or business carried on in Singapore, it is taxable in Singapore upon accrual, regardless of whether it is received in Singapore

When is the deadline for crypto tax in Singapore?

Web3 Individuals

The deadline for filing taxes on cryptocurrency transactions in Singapore aligns with the general tax schedule that runs from January 1 to December 31. Taxpayers must report their taxable income, including any gains from cryptocurrency trading, by April 15 for paper filing and April 18 for e-filing.

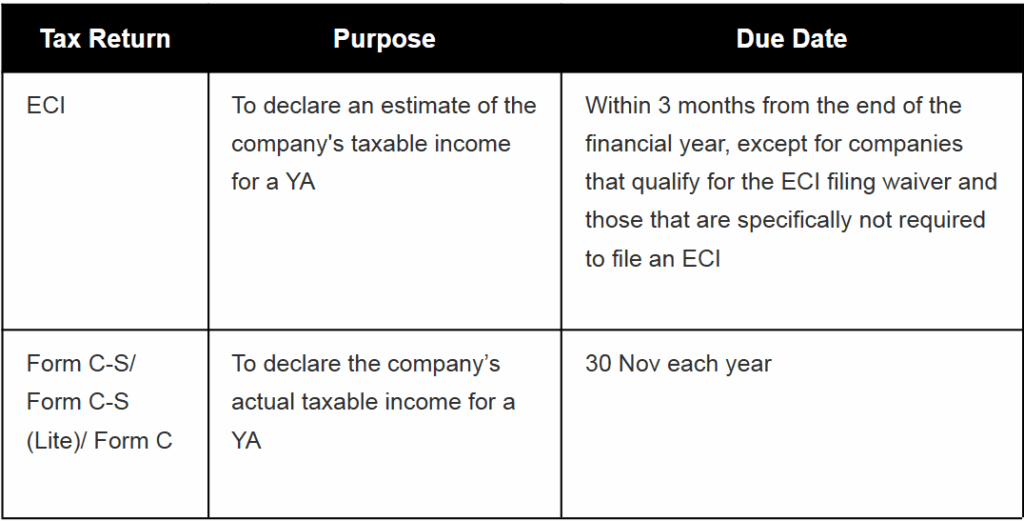

Web3 businesses

How about withholding tax and stamp duty?

With the rise of security/ asset-backed/ RWA/ stablecoins tokens, relevant issuers or holders will need to be aware of withholding tax and stamp duty in Singapore. Generally stamp duty is payable on share transfer in Singapore and Web3 businesses must withhold tax when a payment of a specified nature has been made to non-resident companies/individuals.