IFRS Accounting for Crypto and Stablecoins

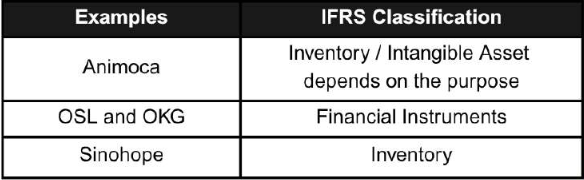

IFRS Accounting Standards do not include a specific standard that addresses digital assets. A company assesses whether a digital asset meets the definition of financial instruments, inventory or intangible assets by applying the scope requirements in the relevant standards and applying the 2019 IFRS IC Agenda Decision.

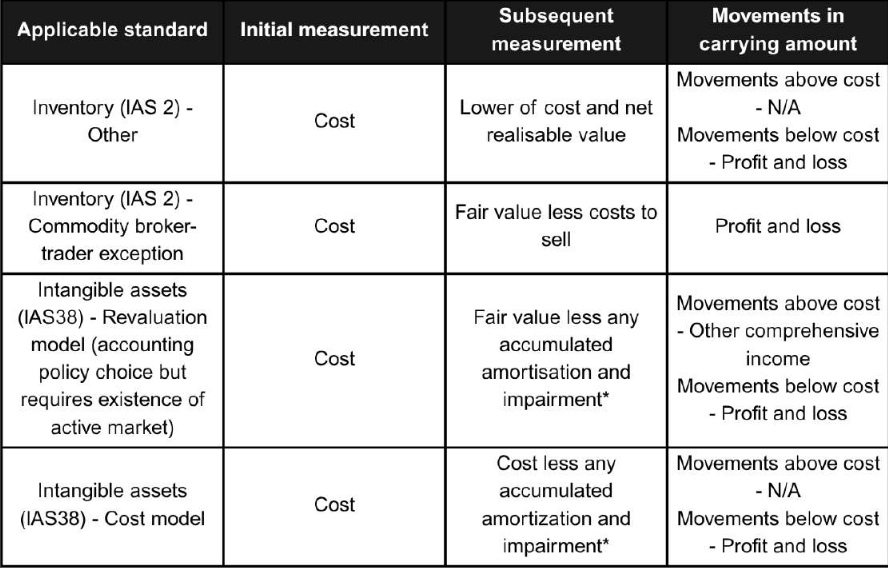

The Committee concluded that such crypto assets do not meet the definition of a financial asset, nor are they cash. However, they could be inventories if held for sale in the ordinary course of business (and measured at the lower of cost and net realisable value), or if acting as a broker-trader of cryptocurrencies, measured at fair value less costs to sell. Otherwise, IAS 38 Intangible Assets applies.

Should crypto held on behalf of customers be on the balance sheet?

In determining whether an asset and liability should be recognised on the balance sheet of the entity holding the cryptographic asset on behalf of customers, an entity considers:

- Whether it has the right (explicit or implicit) to “borrow” the cryptographic assets to use for its own purposes. lf the entity has such a right, it would seem that the definition of an asset set out above is met.

- The rights of customers to cryptographic assets held on their behalf if the entity is liquidated. In particular, if customers would have the status of unsecured creditors with no preferential claim on the cryptographic assets held by the entity on their behalf, this is a strong indicator that the cryptographic assets and the corresponding liability should be recognised on the balance sheet, because the Framework definition of liability would seem to be met.

Segregation of Customers’ assets

The main factors that can be considered include:

- Contract and legal enforceability;

- Asset and transaction reconciliation;

- Traceability of blockchain addresses;

- Location of asset storage;

- Use of hot wallets and cold wallets.

Accounting for stablecoins

Not Cash or Cash Equivalents

Stablecoins are not legal tender, and are generally excluded from cash/cash equivalents under IFRS. They lack the universal acceptability and liquidity typically required.

Digital Asset / Intangible Asset Classification

Most stablecoins are accounted for as intangible assets under current guidance (e.g., IFRS IAS 38).